August 11, 2025

DFWC Q2 KPI Monitor highlights positive shift in staff engagement trends

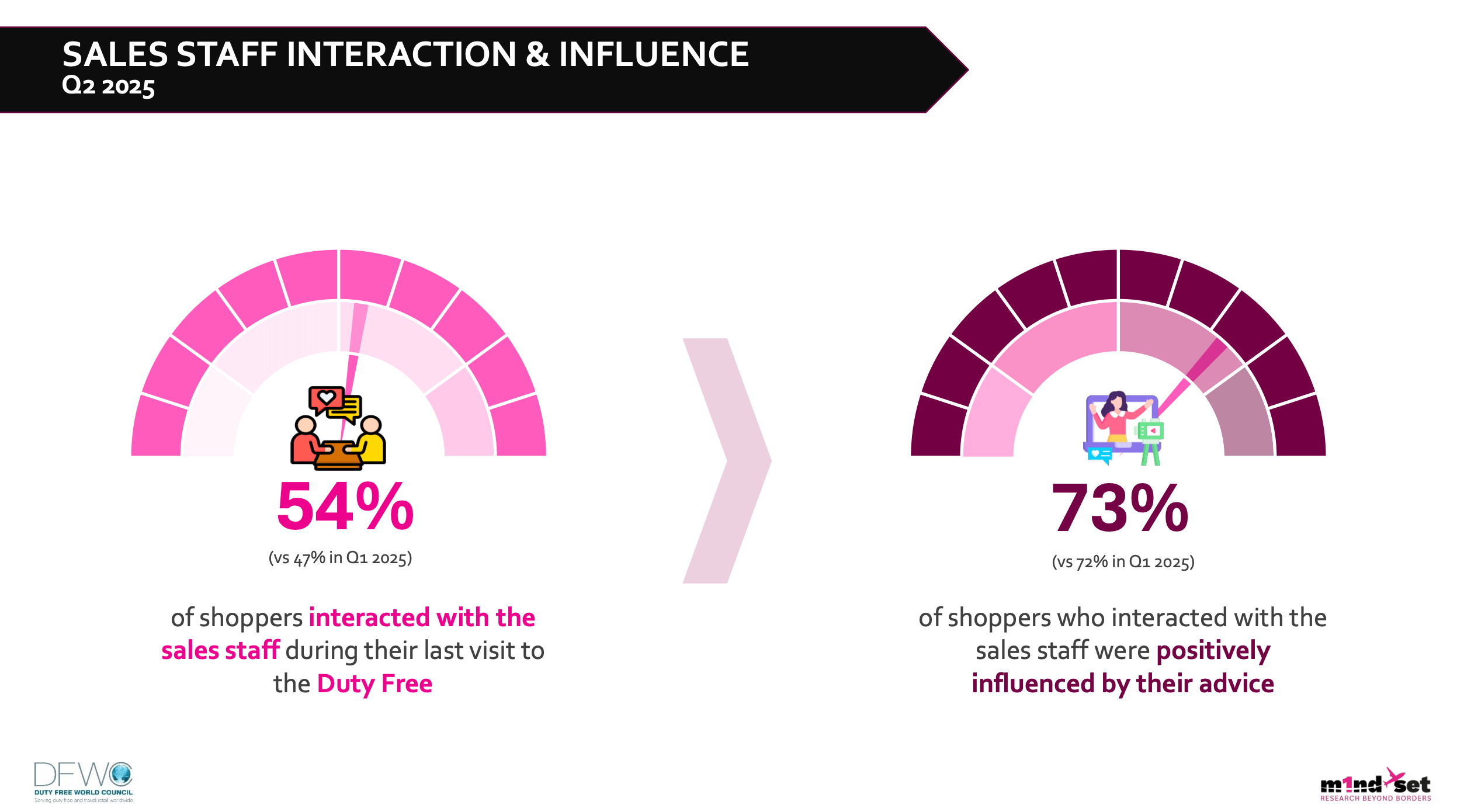

The quarterly KPI Monitor reveals that the proportion of global shoppers who interacted with sales staff rose to 53% in Q2, up from 47% in the previous quarter

The quarterly KPI Monitor, produced exclusively for the Duty Free World Council by Swiss travel and travel retail research agency m1nd-set, reveals that the proportion of global shoppers who interacted with sales staff rose to 53% in Q2, up from 47% in the previous quarter. In addition to the increased frequency of interaction, the quality of these engagements also improved slightly, with 73% of shoppers reporting that the interaction had a positive influence on their shopping experience, up from 72% in Q1.

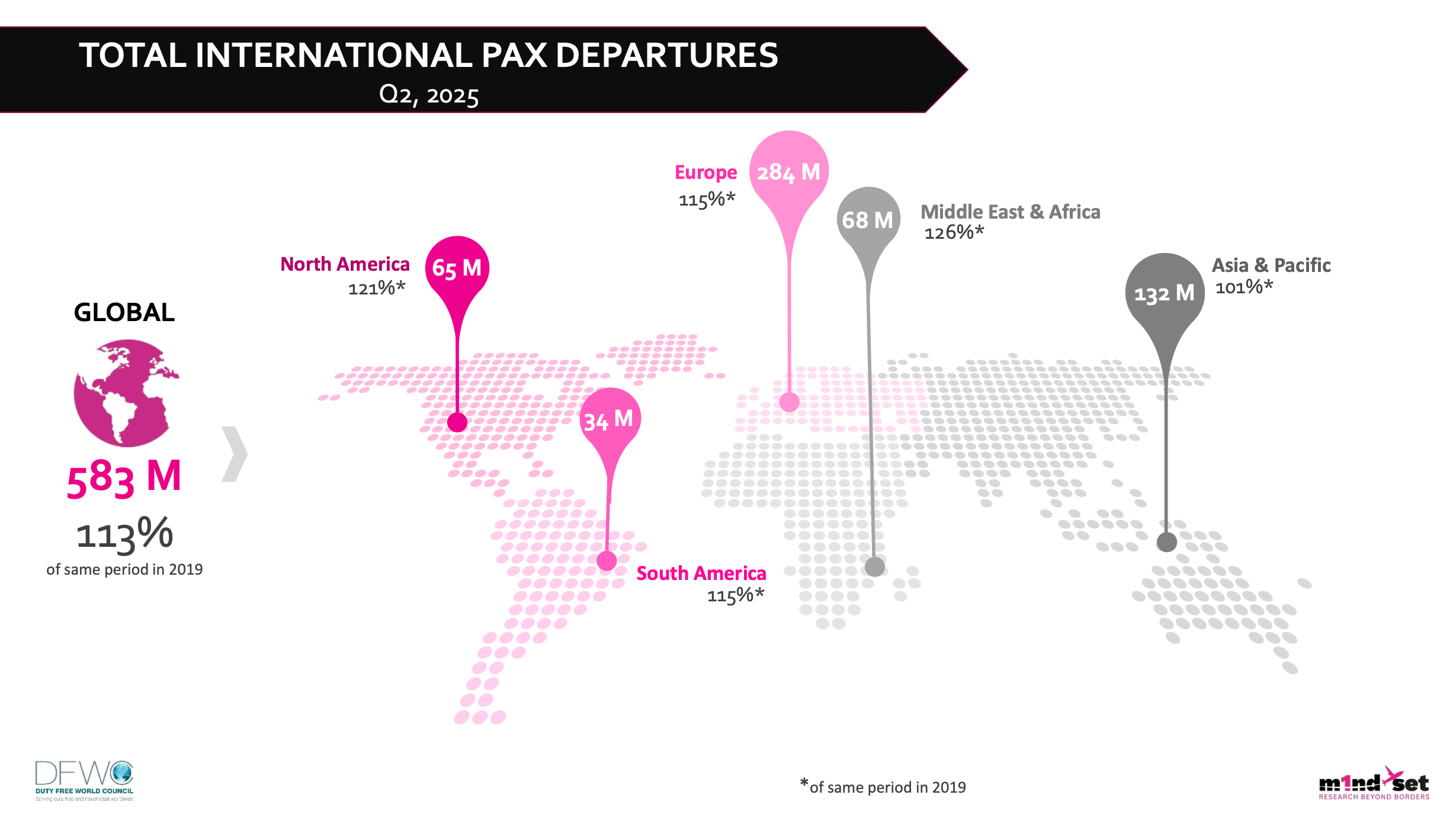

The DFWC quarterly monitor demonstrates that the robust growth in global air traffic reported in the previous quarterly monitor continued in Q2 this year, with 583 million international flights globally, 113% of the level in the same period in 2019. This is also a significant increase, up 15%, on global traffic in the first quarter of 2025. International traffic in Europe surged by just under 40% in Q2 versus Q1 2025, to 284 million flights, also 15% higher than the same period in 2019. In the Middle East & Africa, international traffic was 26% higher than the same period pre-COVID in 2019, at 68 million international flights, but only a marginal 3% increase on Q1 2025 traffic. North America also posted robust growth vs. Q2 2019 with a 21% increase, at 65 million international departures, representing 14% growth on Q1 this year. South America recorded a 15% increase on the same period in 2019 but a 13% drop on Q1 traffic, with 34 million international passengers. Asia Pacific proved to be the least dynamic region in Q2 compared to the same period in 2019, posting only 1% growth to 132 million international departures. However, this was a 6% decline on Q1 2025.

The top 10 nationalities for international departures in Q2 2025 are quasi-identical to the rankings for the first quarter, albeit with a slight reshuffle, and the emergence of Turkey in tenth position. The top three nationalities remain the same, with the US, UK and Germany, each posting 19%, 42% and 35% growth respectively vs. Q1. France moves from sixth to fourth position, edging China into sixth place in Q2, behind India, which remains stable in fifth position. Spain, China, Italy, South Korea and Turkey complete the top ten nationality rankings. With the exception of China and South Korea, which both saw a decline in international departures compared to Q1, all other top 10 nationalities experienced growth on Q1 for international departures, the DFWC reports.

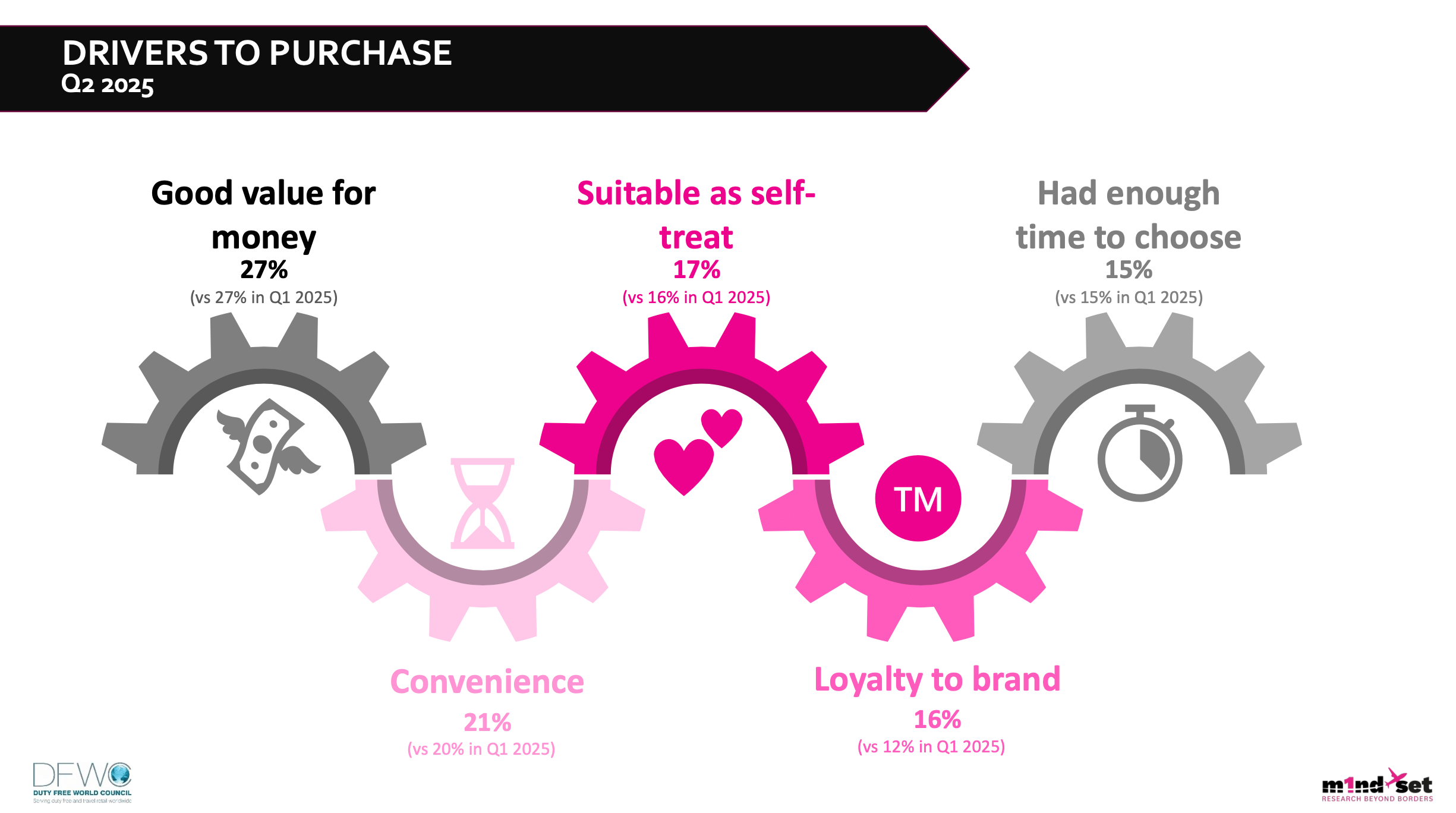

Apart from a notable increase in staff engagement between Q1 and Q2, the DFWC KPI Monitor for Q2 shows minimal variation among global shoppers across most of the other criteria analysed by m1nd-set as part of the Monitor service. The top purchase drivers remain largely consistent in Q2, with “good value for money” (27%), “convenience” (21%), and “suitability as a self-treat” (17%) retaining the top three positions. “Brand loyalty” (16%) rises to fourth place, while “having enough time to choose” (15%) slips to fifth.

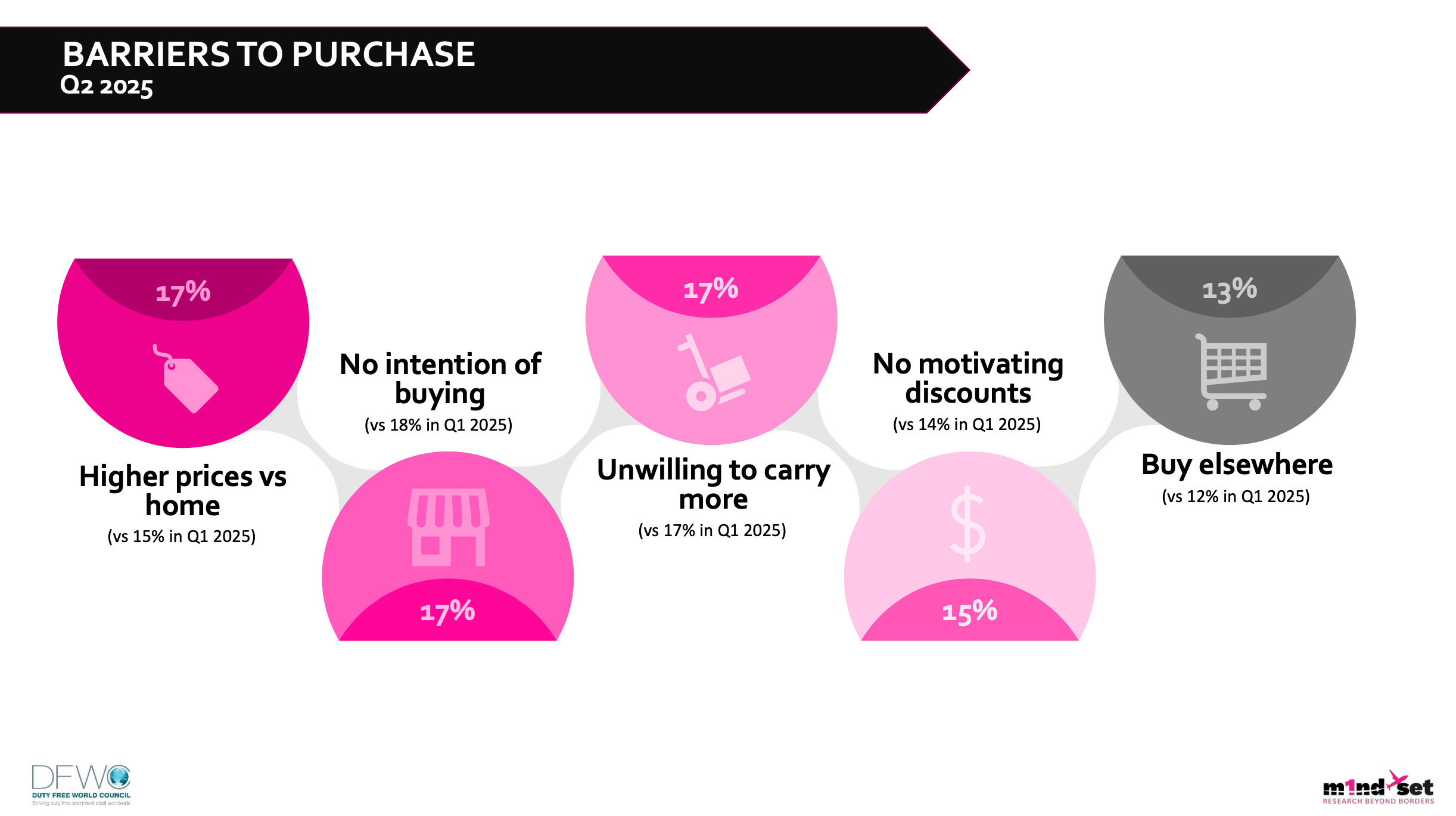

Regarding the main purchase barriers among global shoppers, the top five remain unchanged, though the order has shifted. “Higher prices than at home,” “no intention to buy,” and “unwillingness to carry more items” are tied as the leading barriers at 17% each. “Lack of motivating discounts” (15%) and a preference to “buy elsewhere” (13%) complete the top five.

The purpose of purchase among global travel retail shoppers remained consistent between Q1 and Q2 2025. Over half (53%) continued to buy for themselves, followed by 24% purchasing for gifting, 16% for sharing, and 7% buying upon request.

Purchase planning and impulse behavior showed only slight variation between the two quarters. In Q2, 71% of shoppers planned their purchase, with a modest increase in specific planners from 27% to 28%. Meanwhile, impulse purchases declined slightly from 30% to 29%.

According to the DFWC Monitor, the proportion of global shoppers noticing pre-shopping touchpoints remains stable at 31%. General internet search continues to be the most common touchpoint, cited by 18% of shoppers. Seeing a special promotion ranks second at 13%, followed by proactive searches, either on social media or duty free retailers' websites, both at 12%. Billboard advertising is the fifth most frequently mentioned touchpoint, noted by 11% of shoppers in Q2.

DFWC President, Sarah Branquinho, shares her perspectives on the Q2 KPI Monitor findings: “The Q2 2025 KPI Monitor confirms encouraging signs for our industry, particularly the marked improvement in staff engagement, both in frequency and quality. With over half of global shoppers now interacting with sales staff, and the majority reporting a positive impact, this reinforces the value of human connection in the travel retail experience.”

However, Branquinho continues, “as most shopper behaviors and purchase motivations remain relatively stable, it is clear that more needs to be done to convert traffic growth into sales. We encourage retailers and brands to invest further in staff training and to enhance promotional visibility, especially through digital and in-store channels, to overcome persistent purchase barriers and better capture the attention of today’s travel retail consumers.”

Branquinho adds, “The quarterly DFWC KPI Monitor is possible thanks to our partnership with m1nd-set. By capturing quarterly feedback across all major nationalities, regions, and product categories, and changes in flight and passenger traffic the DFWC monitor provides the travel retail industry with timely, in-depth insights that reflect real-world traveler behavior and seasonal trends.

m1nd-set CEO & Owner Peter Mohn says, “The B1S tracking survey has been the industry’s most consistent and comprehensive source of shopper insights since its launch in 2016, with over 200,000 international travel retail shoppers surveyed to date. B1S compiles data using nationality quotas that are defined based on international traffic data provided by IATA exclusively to m1nd-set, that is representative of the key nationalities that have been travelling internationally during the relevant period of time.

“Even through the disruption of COVID-19, we were able to maintain data quality and representativeness thanks to our exclusive partnership with IATA and our global traveler and shopper panel. We are delighted to service so many industry partners with our shopper analysis and the DFWC through the quarterly monitor."